Stamp duties are taxes levied on legal instruments, used by most governments to raise revenue. Usually, stamp duty laws are dry and boring with most amendments affecting only the amounts of revenue raised by governments from instruments chargeable with stamp duty.

Recently the Malaysian Stamp Act 1949 (“Stamp Act”) was amended by the Finance (No. 2) Bill 2023, passed during the second reading in Parliament on 13 December 2023. The proposed amendments are expected to come into force on 1 January 2024.

Updating of the Stamp Act

The amendments mostly update the Stamp Act for modern day stamp duty practice by removing references to adhesive stamps, postal franking and digital franking machines. More importantly the amendments give legal recognition to electronic instruments for the purposes of liability for stamp duty. This mean that stamp duty will only be payable electronically, and evidence of payment of stamp duty would be generated electronically. The use of adhesive stamps and franking machines have been and will be gradually phased out.

The current practice for submission for adjudication can generally only be done online on the Lembaga Hasil Dalam Negeri’s STAMPS website, with drop down boxes for selection of the relevant provision for the final dutiable amount. Long gone were the days when physical submission of documents involved verbal explanation, and to a certain extent convincing officers, on the basis of stamping under certain provisions of the Stamp Act.

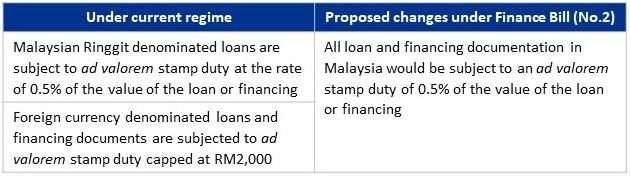

Definitions of “writing” and “written” and removal of ceiling for foreign currency denominated loans and financings

This article addresses two specific amendments which may change the practice of banks and their customers in Malaysia with regards to cross-border foreign currency denominated loans and financings.

These amendments are:

a) Deletion of the RM2,000 ceiling for foreign currency denominated loans and financing documents

This deletion equalizes the stamp duty payable between Ringgit denominated and foreign currency denominated loans and financings.

b) Definition of “written” and “writing” to include electronic documents

Stamp duty on a stampable document executed outside Malaysia is payable within 30 days after the document is first received in Malaysia. With the introduction of the definition of “writing” and “written”, defined to include “any record or transmission which is in electronically readable form”, scanned PDF copies of loan and security documents are technically stampable instruments.

Practical effect of the amendments on international cross border financings

International financings normally involve multiple jurisdictions and loan and security documents being executed and sent across borders.

The net effect of these two amendments are that any loan or financing document, although executed outside Malaysia and denominated in foreign currency, when is sent to Malaysia in electronic form (e.g. by email, or made available for download from a cloud storage), it would be subject to ad valorem stamp duty at the rate of 0.5% of the amount of the loan, payable within 30 days of the loan or security document first being received into Malaysia.

Typically, a Malaysian party to such a transaction would receive the original documents for stamping a few days or weeks after the documents have been signed. The 30-day time period starts running only after the original document is received in Malaysia. There may be days, weeks or even months between the signing of the loan and security documents and the actual drawdown of the loan or financing facility. With the amendments to the Stamp Act, sending a PDF copy of the signed loan or security documents to a Malaysian recipient would start the 30-day clock running.

The net effect of the amendments would be to increase the amount and speed up the collection of stamp duty on loan and security documents executed outside Malaysia, which is probably net positive for the government’s coffers.

Lawyers and bankers would need to be more vigilant the moment the loan and security documents are executed. They must be aware that scanned copies of documents circulated to parties to the transaction may attract Malaysian stamp duty liability when they are sent by email to or made available for download by a Malaysian party.